Rental properties bought at the right price and in the right location are incredible vehicles to take you to financial independence. Overpaying for a rental property and or buying in the wrong location may not work out so well.

There are tons of benefits of owning rental properties. The info below will help you understand the numbers.

In this blog post, I am going to show you how to run some quick numbers when evaluating a rental property. Instead of using in-depth rental property spreadsheets the math I am going to share with you can be done on a scrap piece of paper or back of a napkin.

Why Back Of A Napkin (BON) Analysis?

You may ask yourself why anyone would run the numbers on the back of a napkin for a major investment like real estate? Sounds crazy and risky, doesn’t it?

In reality, this is what most experienced real estate investors do. Instead of wasting tons of time savvy real estate investors do a quick BON analysis to see if a potential deal has promise. If the BON math looks good you can make an offer to get the property under contract subject to inspection and verifying the numbers.

Even Warren Buffett follows the BON principle.

“If you need to use a computer or a calculator to make the calculation, you shouldn’t buy it,” Warren Buffett

Good deals should jump off the back of your napkin and put you into action. If you have to overanalyze the deal using complicated spreadsheets to make the numbers work it probably is a deal you want to pass on.

With the advice of Warren Buffett let’s take a look at how to run the numbers for rental properties.

Gross Rent Multiplier (GRM)

Gross rent doesn’t mean gross as in disgusting. For those of us who collect rent regularly, it’s actually quite delicious:)

Gross rent means the total rent, before subtracting expenses or other deductions. And it’s useful because the gross rent is simple to find and easy to compare to other rental properties.

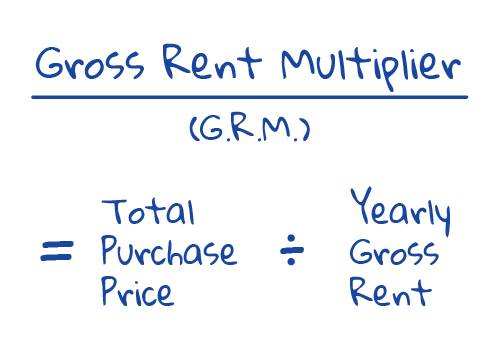

With my back-of-the-envelope snapshot, I begin by using the gross rent to calculate the Gross Rent Multiplier (GRM). The GRM is similar to the Price/Earnings (PE) ratio in stock investing. It’s just a ratio of the property’s total purchase price (including any upfront repair costs) to its yearly gross rent.

Why is the GRM useful? Because it roughly tells us how good a property is at producing income.

For example, a property with a GRM of 12 ($144,000 price / $12,000 rent) is much better at producing income (at least on paper) than a property with a GRM of 20 ($300,000 price / $15,000 rent). The higher the GRM, the less attractive an investment property becomes.

GRM isn’t the only quick analysis I use with gross rental income. A very similar rule of thumb is something called the 1% rule.

The 1% Rule

The GRM is a ratio using yearly rent. But real estate investors usually think in terms of the monthly rent. So, the 1% rule is a rule of thumb that takes that into account.

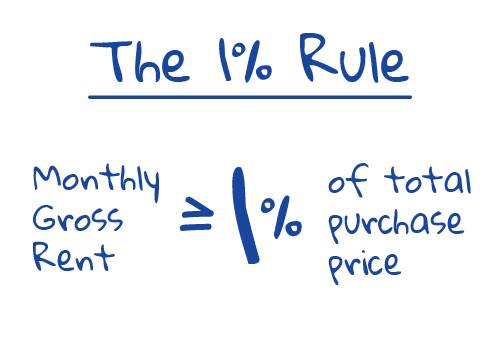

The 1% rule says that the gross rent of a property should equal at least 1% of the purchase costs (or better).

For example, a property with a total upfront cost (price + closing/holding costs + repairs) of $200,000 should at least have a monthly gross rent of $2,000 to meet the 1% rule.

This property that meets the 1% rule would have a Gross Rent Multiplier of 8.33 ($200,000 / $24,000). $24,000 is the annual gross rent, or $2,000 x 12 months.

Meeting the 1% rule does NOT automatically make a deal good. There are properties meeting the 2% rule that you will want to walk away from because of a bad location and rent collection challenges. And properties in high-priced locations will never come close to the 1% rule, yet they still could make financial sense in some cases.

This is a rule of thumb that just allows for quick and easy analysis. If a property DOES meet the 1% rule, it is just one sign that you may have an interesting investment candidate in front of you.

Cap Rate

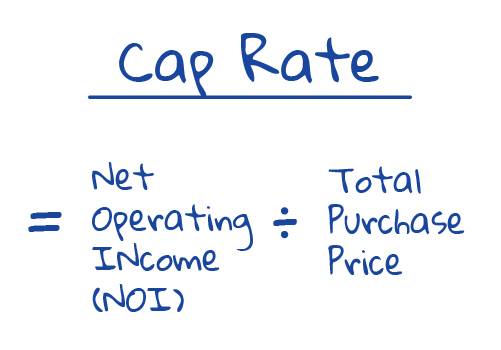

A cap rate is another important income calculation. Unlike the gross rent multiplier, a cap rate tells us how well a property produces income AFTER expenses. Here’s a basic definition:

In case you’re wondering, the Net Operating Income (NOI) is your gross rent MINUS all of the property’s operating expenses and deductions like vacancy, management, taxes, insurance, repairs, HOA costs, etc. These expenses do NOT include financing costs.

For an example of cap rate, let’s say a property produces $6,000 per year in NOI and its total upfront purchase costs are $100,000. $6,000 / $100,000 = a 6% cap rate.

Compare this to another property that produces $7,500 per year in NOI and its total upfront purchase costs are $300,000. $7,500 / $300,000 = a 2.5% cap rate.

One deal produces a 6% unleveraged return (i.e. if there was no debt). The other produces only 2.5%. If all other factors are equal, which deal would move you towards your financial goals faster? The cap rate makes this obvious.

You can use the cap rate as a minimum investment goal. Set a minimum cap rate that you will accept for an investment in a certain location. If the cap rate is below that number, don’t buy it unless you can do something to the property to quickly increase it.

Also, keep in mind that appraisers or brokers of investment properties use cap rates to discuss the overall market. They might say, for example, “the market cap rate is 7%.” This means on average most investors in the market purchase their properties with a 7% cap rate.

The 50% Rule

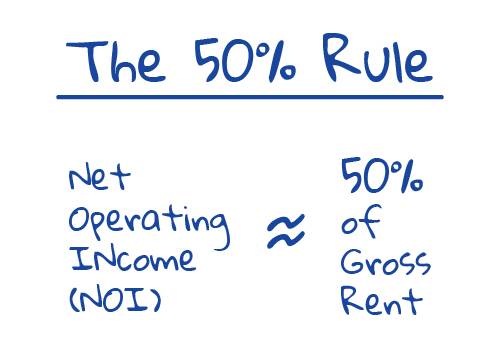

The 50% rule is a shortcut that helps you quickly estimate the NOI and the Cap Rate. But it’s important to remember that it’s just a shortcut and not the final analysis.

This rule of thumb assumes that 50% of your gross rent will be lost to your operating expenses. So, that means your estimated NOI is 50% of the gross rent.

This helps you quickly run the cap rate calculation with your back-of-the-envelope snapshot.

For example, if the yearly gross rent is $18,000, 50% of that is $9,000. If your estimated total purchase investment is $180,000, then your cap rate would be $9,000 / $180,000 = 5%.

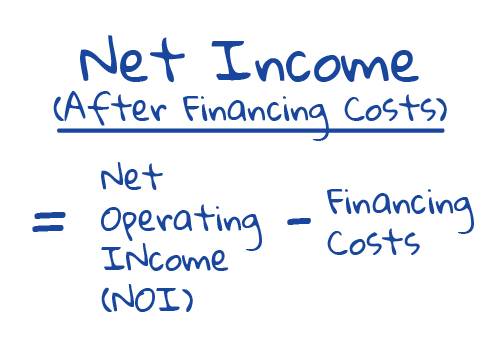

Net Income After Financing Costs

Until now all of our BON income analysis did not take financing into consideration. But many real estate deals DO include financing. So, you will want to know how much rental income is left over AFTER you deduct our financing costs.

Assume you can figure out how to estimate your monthly mortgage payment. If you need a refresher, use this free amortization calculator.

Here is the basic formula for pre-tax net income after financing:

You can set goals for a minimum amount of cash flow you’d like to earn per property. For example, your goal may be to earn a net income of $100/unit. So, a 4-unit property would have to produce a minimum of $400 per month.

This type of goal is useful so that you can ensure your property produces enough regular income to reinvest into one of your real estate retirement plans or to pay for your lifestyle once you’re ready to take it easy.

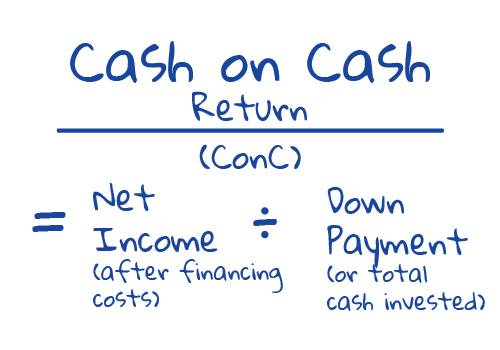

Cash-on-Cash Return

After calculating net income, you run a final income calculation called the Cash-on-Cash (ConC) return. The Cash on Cash Return tells you how much of your down payment or upfront cash investment comes back to you as cash per year. Here is the formula:

If you have a very small down payment (i.e. large amount of leverage), the ConC return is actually not that useful. For example, if you invested $5,000 and earned $400/month, you’d have a 96% ConC return! Or if you invested none of your own money (I’ve done this), the return is infinite – even with minuscule positive cash flow.

While you could use these high ConC returns to brag to your friends, extreme leverage is really what makes this possible. And while I benefited early on from this kind of leverage, just remember that leverage-magnified returns can also lead to leverage-magnified losses! Eventually, you should have more cash to invest in deals if you’re successful.

The ConC becomes more useful when you invest these larger amounts of cash up front. It’s a form of discipline to help you compare your cash return from this deal to other potential investments like bank CDs, bonds, stock dividends, and annuities. Because cash flow is so critical to surviving long-run as a real estate investor, rental investments to make a premium ConC return compared to these other lower-hassle forms of investing. So, if risk-free government bonds return 2%, you want to certainly make a lot more than that.

Like all of these calculations, you have to also look at the entire picture. If you’re making huge returns on the property’s equity, for example, it might be acceptable to have a smaller or even a negative ConC return for a short period of time. But in an ideal world, you’d make acceptable returns with all calculations.

Now that we’ve covered the BON analysis for calculation #1 – income, let’s continue and look at calculation #2 – equity.

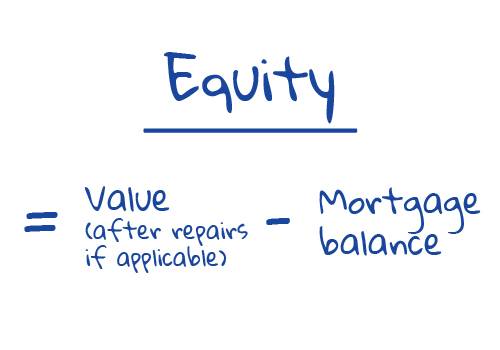

Equity – Rental Property Calculation #2

Equity is a financial term for what you own. Maybe you’ve heard equity used to describe shares of stock in a company, but equity can also be calculated for a real estate property. What you “own” is the difference between the fair market value of the property (your asset) and the balance of any debt (your liability).

Calculating equity is simple. The math is like this:

There are two numbers you must know for this simple math, the value and the mortgage balance.

This DYI valuation process is not a replacement for expert help from an appraiser or experienced real estate agent.

The ARV process explained in that article also assumes you’re buying a house or small multiunit that is best valued with comparable sales. If you’re buying a larger income property that obtains its value from the income approach to value, you’ll want to use that process (and certainly get a second opinion). Here’s a good example of the income approach to valuation in action.

The mortgage balance calculation is more straightforward. For the present balance, you’ll just use the amount you’re borrowing. For a future mortgage balance, you can just use an amortization schedule.

Conclusion

This article is about quickly running the numbers when evaluating rental properties so you can analyze more deals.